Email

Email Print

Print

Chemical Tankers Market Overview

The Chemical Tankers Market size is forecast to

reach US$35.6 billion by 2027, after growing at

a CAGR of 4.1% during the forecast period 2022-2027. Chemical tankers are cargo

ships used for the transportation of liquid chemicals in bulk. Chemical tankers

range from 5,000 to 59,000 deadweight tonnage (DWT) in size and have cargo tanks that

are either coated with epoxy or zinc paint or made from stainless-steel.

Chemical cargoes carry chemicals such as caustic

soda, sulfuric acid, methanol, many other organic inorganic chemicals, all

of which may be hazardous. Based on the hazards, chemical tankers

are designed, constructed and operated to mitigate the risks. In order to transport

goods, chemical tankers are also classified based on the International Maritime

Organization (IMO) hazard classification of either type I, II or III. The

increasing global economic activity acts as a driver for the Chemical Tankers Market.

Chemical Tankers Market COVID-19 Impact

The COVID-19 pandemic has disrupted every sphere of

life, led to restrictions on the movement of goods at the domestic as well as

international levels. Ports were closed due to quarantine which crippled the

shipping industry. Vessels from certain countries were not allowed to dock due

to fear of contamination. The challenges of crew rotations to mitigate the

spread of the virus quickly grew into a crisis for the global shipping

industry. The pandemic disrupted maritime shipping services, leading to

canceled sailings, port delays container shortages. These disruptions were

particularly profound for imports originating from North-East Asia. Combined

with COVID-related changes, the disruptions increased volatility in maritime

freight rates across regions caused significant delays in the delivery of

crucial imports. According to the International Trade Commission, in the first

half of 2020, US maritime container imports declined 7% by volume, compared to

the same period in 2019. Container shipping firms canceled more than 1,000

voyages in the first six months of 2020. The pandemic wreaked havoc across the

shipping industry resulted in cargo delays, shipping container shortages high

freight prices; which impacted the Chemical Tankers Market as well.

Report Coverage

The “Chemical Tankers Market Report – Forecast

(2022-2027)” by IndustryARC, covers an in-depth analysis of the

following segments of the chemical tankers industry.

Key Takeaways

- Asia-Pacific dominates the Chemical Tankers Market on account of the established chemical industry in the region. According to Invest India, the chemicals & petrochemicals sector is expected to grow to US$300 billion by 2025.

- Chemical tankers are vessels that are used to carry liquids in bulk, from methanol to vegetable oils.

- Based on the chemicals transported, different types of coatings are used for the tanker. For instance, edible crude vegetable oils require epoxy coating. Acids and other harsh chemicals are transported in stainless-steel tankers. Some tankers also have zinc coating.

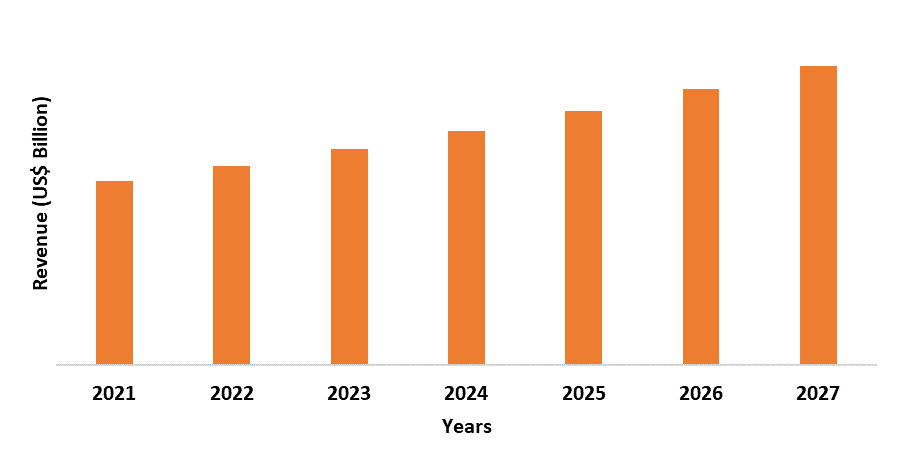

Figure: Asia-Pacific Chemical Tankers Market Revenue, 2021-2027 (US$ Billion)

For More Details On this report - Request For Sample

Chemical Tankers Market Segment Analysis – By Cargo

The IMO II segment held the

largest share in the Chemical Tankers Market in

2021. Chemical tankers may carry dangerous, flammable, toxic chemicals. In

order to transport goods, chemical tankers need to have the proper International Maritime Organization (IMO) hazard

classification of either type I, II or III. A type I chemical tanker is

intended to transport most hazardous chemicals, requiring maximum preventive

measures to prevent any leakage of cargo. Type II chemical tanker is intended

to transport chemicals requiring significant preventive measures whereas type

III chemical tanker is intended to transport chemicals requiring a moderate

degree of containment to increase survival capability in a damaged condition.

Most chemical tankers are IMO II III since the volume of IMO I cargoes is

limited. The growth of the IMO II cargo segment of the chemical tankers is

because of the use of IMO II chemical tankers for shipping chemicals such as methanol,

ethanol, vegetable oils, fats, along with alkanes. Therefore, this segment is

anticipated to dominate the Chemical Tankers Market.

Chemical Tankers Market Segment Analysis – By Material

The stainless-steel segment held

the largest share in the Chemical Tankers Market is expected to grow at a CAGR

of 3.9% during the forecast period. Chemical tankers are generally equipped

with a series of separate cargo tanks that are either coated with specialized

coatings such as epoxy or zinc paint or made from stainless-steel.

The coating or cargo tank material determines what types of cargo a particular

tank can carry. For instance, stainless-steel tanks are required for aggressive

chemicals such as sulfuric acid, phosphoric acid, other aggressive organic

inorganic chemicals. Stainless-steel is widely used as a tank material owing to

its better chemical resistance and greater ease in tank cleaning inspection.

Thus, cargo contamination hazards can be reduced in stainless-steel tankers.

This is the reason why a majority of the chemical tankers have stainless-steel

tanks. For instance, the IINO Lines website states that 74.4% of the group’s

chemical tanker fleet is equipped with stainless-steel tanks. Therefore, the stainless-steel

segment is set to dominate the market during the forecast period.

Chemical Tankers Market Segment Analysis – By Geography

The Asia-Pacific region held the largest share in

the Chemical Tankers Market in 2021 up to 46% due to the region's

well-established agriculture chemical sectors. Palm oil forms the largest cargo

group within the vegetable oil sector. India is the world’s second-largest

consumer number one importer of vegetable oil. As per the Economic Survey

2021-22, India imports around 60% of its consumption of edible oils, palm oil

constitutes around 60% of the imports of edible oils. According to the Solvent

Extractors Association of India (SEA), India imported around 1 million tonnes

of edible oil in March 2022 when compared to around 0.9 million tonnes of

edible oil in March 2021. Indonesia and

Malaysia account for 85% of the global production of edible oils. According to government sources, Malaysia is planning to boost its share of the edible oil market after geopolitical tensions due to the Russia-Ukraine war disrupted sunflower oil shipments further tightened global supplies. Japan, Korea, China are major shipbuilding yards. Currently, a majority of the world’s stainless-steel chemical tankers are from these three countries. Therefore, this region is expected to continue to dominate the Chemical Tankers Market.

Chemical Tankers Market Drivers

Increasing Global Economic Activity Post-Pandemic

The pandemic caused severe damage for the global

shipping industry. However, once the lockdown was lifted, the revival of the

economy began. The global economy is dependent on chemicals, as every industry,

directly or indirectly, requires chemicals. For example, chemical tankers carry caustic soda which is

required in the processing of bauxite to make aluminum. Transportation of

chemicals by sea is a cost-efficient, fast, effective method of cargo delivery

over long distances. According to the World Bank, the global economy is poised

to stage its most robust post-recession recovery in 80 years, in 2021, ever

since the onset of the pandemic. The emergence of vaccines has also given a

positive outlook for the global economy. For instance, the US economy has been

bolstered by massive fiscal support, vaccination is expected to become

widespread by mid-2021, growth is expected to reach 6.8% in 2021. As the

vaccination rates increased, several countries began easing restrictions which

opened up more shipping routes. Chemical tankers carry hazardous chemicals that

are crucial in the synthesis of pharmaceuticals which are in high demand due to

the pandemic. The demand for chemicals in the next couple of years will be

driven by an expected strong recovery following the pandemic across the globe.

Therefore, the increasing global economic activity drives the Chemical Tankers Market.

Change in Trade Flows

After the pandemic slump, global trade rebounded in

2021 is expected to recover further in 2022. According to the United Nations

Conference on Trade Development (UNCTAD), in Q1 2021, the value of global trade

in goods services grew by about 4% quarter-over-quarter by about 10%

year-over-year. Global trade in Q1 2021 was higher than pre-crisis levels, with

an increase of about 3% relative to Q1 2019. Europe relied on Russian exports

for methanol, caustic soda, benzene, styrene. Due to the invasion of

Ukraine, several countries including European countries, imposed sanctions on

Russia stopped Russian exports. As Russian exports are mainly short-haul,

replacement volumes will add additional miles therefore drive tonnage demand

higher. However, other countries in Asia have not halted Russian exports

leading to incremental demand in tonnage an increase in miles. Thus, change in

trade flows is a driver for the Chemical Tankers Market.

Chemical Tankers Market Challenges

Volatility of Crude Oil Prices

Maritime vessels use bunker fuel to power their motors. Despite the International Maritime Organization (IMO) announcing a 0.50% global sulfur cap on marine fuel emissions from January 2020, the fuel maritime vessels run on is obtained from crude oil. Therefore, crude oil prices directly affect the chemical tankers industry. The US-China trade war in 2019 resulted in a large crude oil price drop. In August 2019, U.S. West Texas Intermediate (WTI) crude fell US$1.18, or 2.1%, to US$54.17 a barrel. On 20 April 2020, the price of WTI crude oil slumped into negative for the first time in history, falling to negative US$37.63 per barrel. The Texas Freeze in February 2021 also impacted crude oil prices. WTI crude fell 62 cents, or 1%, to settle at US$60.52 a barrel. On February 24, when US President, Biden, announced sanctions against Russia, WTI crude rose 71 cents, or 0.8%, to settle at US$92.81 a barrel, after earlier rising to US$100.54. As Russia is the world's second-largest producer of crude oil after Saudi Arabia, supplies about a third of Europe's needs, the geopolitical tensions directly affect crude oil prices. On 6 March 2022, the US Secretary of State said that the US administration its allies were discussing a ban on Russian oil supplies. This led to a jump in oil prices to US$139 a barrel. Due to the ongoing geopolitical tensions, crude oil prices skyrocketed in international markets as WTI reached US$120 a barrel. As of June 2022, WTI crude settled at $120.26 per barrel. Thus, the volatility of crude oil prices poses a challenge for the Chemical Tankers Market.

Chemical Tankers Industry Outlook

Product launches, acquisitions and R&D activities are key strategies adopted by players in the Chemical Tankers Market. The Chemical Tankers top 10 companies include:

- Stolt-Nielsen

- Odfjell

- Navig8 Chemicals

- Wilmar International

- Mitsui O.S.K. Lines

- IINO KAIUN KAISHA, LTD.

- Tokyo Marine Asia Pte Ltd

- Nordic Tankers

- Seatrans Chemical Tankers

- Bahri Chemicals

Recent Developments

- In November 2021, Odfjell announced that it disposed of its last short-sea vessels in the Asia-Pacific market to focus on its core deep-sea chemical tanker business.

- In November 2021, BW Group’s Hafnia Ltd. announced that it is acquiring a fleet of 32 IMO II tankers from Oaktree Capital Management’s Chemical Tankers Inc.

- In July 2021, IMC’s Aurora Tankers formed a partnership with Golden Stena Baycrest Tankers to manage operate stainless-steel chemical tankers. The partnership aims to focus on expansion across Asia for the two companies.

Relevant Reports

Flexitank Market-

Forecast (2022 - 2027)

Report Code: CMR 53325

Shipping Containers Market- Forecast (2021 - 2026)

Report Code: AM 87656

Cargo Shipping Market- Forecast (2021- 2026)

Report Code: AM 31693

For more Chemicals and Materials Market reports, please click here